| “The spread between value and growth has reached a point historically associated with a reversal; the Russell 1000 value index is up 9 percent this year, against a gain of 27 percent in the comparable growth index. Tax reform is a catalyst for a rotation into value stocks, as value companies generate almost 80 percent of their revenue in the U.S. and are subject to an effective tax rate of 30.3 percent, the strategist observes.” |

Tax reform isn’t the only driver that may support value stocks. Value also tends to outperform when interest rates are rising. If the Federal Reserve has anything to say about, rates should begin to move higher.

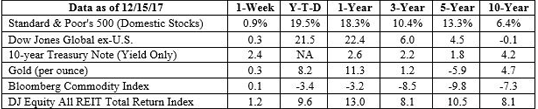

The Federal Open Market Committee (FOMC) increased its benchmark interest rate by one-quarter of a percentage point last week. It was the third increase during 2017.

Normally, a Fed rate hike would be expected to push Treasury rates higher; however, that didn’t happen last week. Rates on U.S. government bonds fell on Wednesday after the Fed took action, reported CNBC. It’s notable that, after three rate hikes during 2017, the yield on 10-year Treasury bonds finished last week at 2.4 percent, which was lower than at the start of the year.

Following the FOMC meeting last week, Chair Janet Yellen told CNBC, “My colleagues and I are in line with the general expectation among most economists that the type of tax changes that are likely to be enacted would tend to provide some modest lift to GDP growth in the coming years.”

A lot of folks are scratching their heads wondering when inflation is going to move higher. The Fed has been expecting it to happen for a while. Maybe 2018 will be the year.

Here’s Another Reason To Like Emerging Markets

The MSCI Emerging Markets Index was up more than 30 percent year-to-date late last week, outperforming national indices in most developed nations. (Remember, past performance is no indication of future results.) There may be more to like about emerging markets than 2017 performance, though, wrote Ben Inker in the latest GMO Quarterly letter:

| “…if there is one group of equities that deals with inflation on a pretty much continuous basis, it is emerging equities…To be clear, our fondness for emerging equities today is driven overwhelmingly by their cheaper valuations…But if worse did come to worst and inflation flared up, owning a good chunk of the only equities that remember what inflation is like seems like a decent idea.” |

Do you remember inflation?

In the 1970s, it was a household name. People wore WIN (Whip Inflation Now) buttons, earrings, sweaters, and other paraphernalia after President Ford declared inflation “public enemy number one.” The Great Inflation, as it was called, lasted from 1965 to 1982 with inflation rising above 14 percent in 1980.

While another Great Inflation isn’t expected, it’s likely inflation eventually will move higher. For most of the last decade, inflation in the United States has remained low. As economic activity picked up, late in 2016 and early in 2017, the pace of inflation increased and moved slightly above the Federal Reserve’s target level of 2 percent. Then, it dropped once again, reported Inker.

Goldman Sachs recently suggested “a sizable and relatively long-lasting drag from the earlier weakness in import and commodity prices…” is the reason for low inflation, and the company anticipates inflation will increase during 2018.

If inflation begins to move higher, the Federal Reserve is likely to continue to push interest rates higher. Higher interest rates translate into higher bond yields and that could affect investors by making investments with lower risk more attractive.

We hope you will enjoy a very happy holiday!]]>