| “…a range of stock benchmarks made their biggest single-day fall since November, as the political controversy over Donald Trump ties with Russia undermined investors’ faith in the administration’s ability to enact its pro-growth policies. Markets subsequently steadied, but investors are primed for further volatility as the White House faces the distraction of a lengthy inquiry led by an independent special counsel.” |

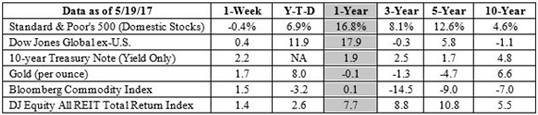

Markets recovered some ground late in the week as the influence of Washington, D.C. drama was offset by strong earnings news. On Friday, FactSet reported first quarter earnings results were in for 95 percent of the companies in the Standard & Poor’s 500 (S&P 500) Index and 75 percent had beaten estimates. Altogether, corporate earnings were about 6.0 percent higher than expected.

Earnings performance was particularly strong for companies in the Information Technology, Healthcare, and Financials sectors, and relatively weak for companies in the Telecom Services, Real Estate, and Consumer Staples sectors.

Brace yourself. Next week may be bouncy. The Federal Reserve Open Market Committee will release minutes from its most recent meeting. In addition, we’ll receive the administration’s proposed budget, along with new economic data and consumer sentiment readings.

Are You Helping Your Adult Children Financially?

In 2015, Pew Research investigated whether aging parents received more assistance from adult children or adult children received more assistance from parents. In the United States, Italy, and Germany, they found parents provide more financial assistance to their adult children than the adult children provide to their parents.

The survey found 39 percent of American parents had helped their adult children with errands, housework, or home repairs during the past twelve months, and 48 percent had helped with childcare. Almost two-thirds had provided monetary support. Financial help appeared to be contingent on parents’ circumstances. Those with higher household incomes were more likely to give money to adult children.

Becoming the ‘Bank of Mom and Dad’ can be a slippery slope, according to AARP Magazine. Since parent-child relationships can be emotionally fraught, it’s sometimes difficult to gauge when financial assistance is a good idea and when it’s not. Should you pay for a car repair? Help with the down payment on a home or apartment? Foot the bill for a grandchild’s private school or college? Fund a lavish wedding? Help with medical bills?

The AARP suggested answering four questions, using a scale of 0 to 5, may help parents determine whether to give money to an adult child. The questions are:

1. Will this investment add stability and security to my child’s life?

(0 = entirely optional; 5 = absolutely necessary)

2. Is this a short-term or one-time cash need, or is it something that could go on for years? (0 = guaranteed, long-term payouts; 5 = absolutely just one time)

3. Is there risk in the investment beyond the cash outlay, such as financial liability on a contract or damage to your credit?

(0 = very high levels of risk; 5 = no additional risks)

4. Can you lend or give this money without fear of damaging your relationship with your child? Or, will it cause tensions or resentments for the people involved? (0 = guaranteed tensions or resentments; 5 = everyone is happy)

If the combined answers total 13 or higher, the answer is yes, give money to your adult child. If the total is less than 13, you may want to think twice before opening your wallet.]]>