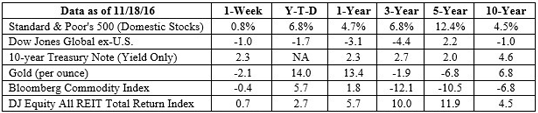

“BofA ML [Bank of America Merrill Lynch] said the weekly influx was the biggest into equities since December 2014. The outflows from bonds, meanwhile, was the largest since the taper tantrum of June 2013…The flight from bonds made for the biggest two-week loss in more than a quarter-century in the Bloomberg Barclays Global Aggregate Index, which fell some 4 percent, Bloomberg reports. The outflows from municipal and emerging market bond funds were especially acute, about $3 billion and $6.6 billion, respectively.”

The Wall Street Journal reported the yield on 10-year U.S. Treasuries finished last week at a 12-month high, after recording the biggest two-week gain in 15 years.

Will investors’ enthusiasm for U.S. stocks persist? Will this prove to be the end of the 35-year bull market in bonds? Stay tuned.

Looking For A Great Gift?

If you have friends or relations with young children, consider starting or contributing to a 529 College Savings Plan. It’s a great way to fund a future education and, let’s face it, really young children often enjoy the box and wrapping more than the gift.

So, if you want to give a child something they’ll always remember, starting a college fund may fit the bill. It’s a gift that may also benefit the parents. The College Board reported the average cost of tuition, fees, room, and board for in-state students attending a public four-year university is expected to be about $20,000 for the 2016-17 school year. At that rate, the average cost for four years of college would be about $80,000. Since two-thirds of students received financial aid during the 2014-15 school year, the following example estimates out-of-pocket college costs at $60,000.

Consider the cost of each option for this fictional family:

- Borrowing to pay for college: The Smiths borrow $60,000 to pay for 18-year-old Joe Smith’s college tuition. The interest owed is 5 percent per year. Over the next 10 years, they repay the principal, plus about $16,400 in interest. By the time Joe is 28, and the loan is repaid, his undergraduate degree will have cost about $76,400.

- Saving to pay for college: Alternatively, the Smiths could open a 529 Plan account for Joe Smith when he was born. If his family contributed $2,100 a year to the account and earned 5 percent each year, at age 18, Joe would have about $62,000 for college. His family would have contributed about $37,800 and earnings in the account would have contributed about $24,200.

The difference in the amount this fictional family would spend on college is about $38,600.

529 plans offer other advantages, too. Any earnings plan accounts grow federally tax-free, and distributions are tax-free as long as the money is used for qualified college expenses. Many states offer tax deductions or tax credits for 529 plan contributions, as well.

Any adult can open a 529 plan and fund it on behalf of a child. Once the account has been established, parents, grandparents, relatives, and friends can contribute. If you would like to learn more, contact your financial professional.

]]>