Market Insights:

January 2, 2024

Posted on January 02, 2024

Planning and Guidance, Tailored To Your Life and Goals

Tuesday Takeaway

Posted on April 21, 2020

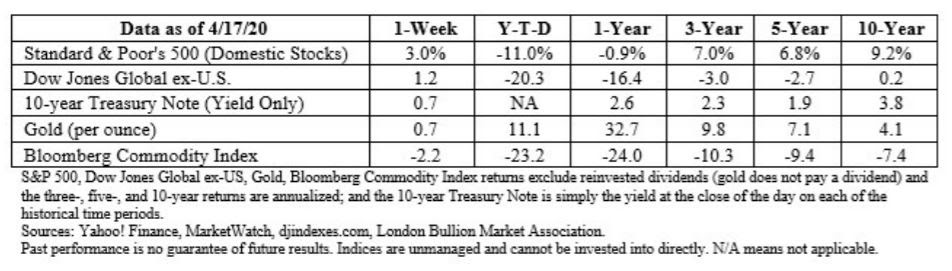

The Markets

Job loss is painful in any circumstances. It’s particularly intimidating when it occurs in the midst of a pandemic and economic downturn. If you are recently unemployed, here are five things you can do:

1. Review your health insurance options. You may have the option to keep your employee health plan for a period of time. It’s temporary and it can be expensive. You pay the entire premium, including the amount your employer used to pay. It may be less expensive to join a spouse’s plan if that is an option. Another alternative is to purchase a plan through the Health Insurance Marketplace. Losing a job qualifies you for a special enrollment period.

2. Get financial advice. We’ll help you evaluate your financial position by reviewing monthly expenditures and available cash, so you know how long you can make ends meet with current financial resources. It may be possible to reduce monthly spending relatively quickly. Banks, credit card companies, and other institutions are allowing customers who call to defer payments because of COVID-19 shutdowns.

3. File for unemployment benefits. Ratchet up your patience. State unemployment benefit systems have been overwhelmed by the sheer number of applicants. Completing online forms and filing for weekly payments can take a significant amount of time, so file as soon as you can and be patient.

4. Update your resume and LinkedIn profile. Revamp your resume. Polish your LinkedIn profile. Make sure your profile is ‘public’ so people can find you. Join groups that share your interests and passions. Learn more about companies you may want to join.

5. Reach out. Start connecting with friends and colleagues. Let them know you are looking for your next opportunity.

Consider doing volunteer work or freelancing until you find a new position. Work of any kind will help you stay busy during the times you’re not hunting for a new job.]]>

Job loss is painful in any circumstances. It’s particularly intimidating when it occurs in the midst of a pandemic and economic downturn. If you are recently unemployed, here are five things you can do:

1. Review your health insurance options. You may have the option to keep your employee health plan for a period of time. It’s temporary and it can be expensive. You pay the entire premium, including the amount your employer used to pay. It may be less expensive to join a spouse’s plan if that is an option. Another alternative is to purchase a plan through the Health Insurance Marketplace. Losing a job qualifies you for a special enrollment period.

2. Get financial advice. We’ll help you evaluate your financial position by reviewing monthly expenditures and available cash, so you know how long you can make ends meet with current financial resources. It may be possible to reduce monthly spending relatively quickly. Banks, credit card companies, and other institutions are allowing customers who call to defer payments because of COVID-19 shutdowns.

3. File for unemployment benefits. Ratchet up your patience. State unemployment benefit systems have been overwhelmed by the sheer number of applicants. Completing online forms and filing for weekly payments can take a significant amount of time, so file as soon as you can and be patient.

4. Update your resume and LinkedIn profile. Revamp your resume. Polish your LinkedIn profile. Make sure your profile is ‘public’ so people can find you. Join groups that share your interests and passions. Learn more about companies you may want to join.

5. Reach out. Start connecting with friends and colleagues. Let them know you are looking for your next opportunity.

Consider doing volunteer work or freelancing until you find a new position. Work of any kind will help you stay busy during the times you’re not hunting for a new job.]]>

Posted on January 02, 2024

Posted on December 18, 2023

Posted on December 11, 2023

Posted on December 04, 2023