Market Insights:

January 2, 2024

Posted on January 02, 2024

Planning and Guidance, Tailored To Your Life and Goals

Tuesday Takeaway

Posted on March 17, 2020

The Markets

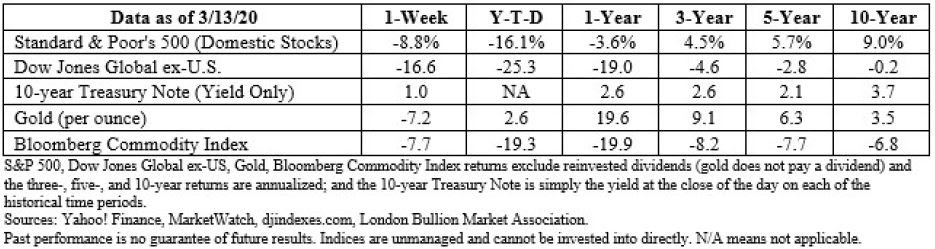

Last week was one for the history books.

Mid-week, the World Health Organization (WHO) declared coronavirus a global pandemic. At the time, there were more than 118,000 cases in 114 countries, and the death toll exceeded 4,000 people. On Friday, the Centers for Disease Control (CDC) reported 46 states and the District of Columbia have been affected, so far. As of Friday, there have been 1,629 confirmed and presumptive cases and 41

deaths.

As the need for containment became clear, daily life underwent rapid change. Major gatherings, from sporting events to Broadway shows to industry conferences, were canceled. Travel was restricted. Schools closed or moved to online classes. Restaurants and bars began serving fewer customers. Many Americans began working remotely or, in some cases, not working at all.

Uncertainty about the economic impact of the virus contributed to stock market volatility. Major American stock indices dropped into a bear market territory, last week. Bear markets occur when prices drop by 20 percent or more from recent highs. Peter Wells of Financial Times reported:

“…a combination of fears stemming from the coronavirus pandemic, oil price plunge, and a global recession killed off an 11-year bull market. Wall Street’s equities benchmark plunged 9.5 percent on Thursday, its biggest one-day drop since Black Monday in October 1987 and also its fifth-biggest one-day drop since 1928.”

On Friday, President Trump declared the coronavirus a national emergency. Reshma Kapadia of Barron’s reported the declaration freed up $50 billion to support local, state, and federal efforts. It also “…grants new authorities to the Health and Human Services department, and gives doctors and hospitals greater flexibility to respond to the virus and care for patients…”

All three major U.S. stock indices rallied after the national emergency declaration, but it wasn’t enough to recover losses from earlier in the week. Chuck Mikolajczak of Reuters reported:

“The indexes were still about 20 percent below record highs hit in mid-February, and each saw declines of at least 8 percent for the week. Since hitting the highs, markets have been besieged with big swings in the market, nearly matching as many days with declines of at least 1 percent as all of 2019. Friday’s surge was the biggest one-day percentage gain for the S&P 500 since October

28, 2008.”

On Saturday, the House passed a bipartisan economic stimulus and relief bill to provide support while the coronavirus is being contained. It is expected to pass the Senate next week, reported Erica Werner, Mike DeBonis, Paul Kane, and Jeff Stein of The Washington Post. The current legislation is separate from the $8.3 billion emergency spending bill passed two weeks ago.

The CBOE Volatility Index (VIX), which is known as Wall Street’s fear gauge, traded above 50 every day last week. At the start of the year, the VIX was trading at 12.47, and it has averaged 22.05 during 2020 to date, reported Macrotrends. A high VIX reading indicates traders anticipate markets will remain volatile.

Recent bouts of volatility appear to have been caused by institutional trading rather than individual investors. Abby Schultz of Penta reported:

“…individual investors are largely sitting tight, according to survey data from Spectrem Group in Chicago. About three-quarters of investors with $100,000 to $25 million in investable assets who were surveyed between Wednesday, March 4…and Monday, March 9 … did not change their investment portfolios at all in light of the market sell-off…Among those with $5 million to $10 million in investable assets, as well as those with $10 million to $15 million, 31 percent bought stocks in the last 20 days…Among those with $15 million to $25 million, 39 percent bought stocks…”

[/caption]

While southern migration has played a role in many retirements, the Milken Institute suggests today’s retirees may be seeking a different type of retirement experience. “They are launching companies and nonprofits, climbing mountains, creating apps, and mentoring youth. They increasingly seek lifelong engagement and purpose.”2

Often, older Americans are finding these experiences close to their hometowns. While many retirees move, most – 60 percent on average – land within 20 miles of their previous homes. They tend to remain close to family and friends and age in familiar communities. Just one-fifth move more than 200 miles away, according to the Center for Retirement Research at Boston College.3

Those who settle farther from home may choose their destinations because they offer engaging programs and valued amenities. In its 2017 report on the Best Cities for Successful Aging, the Milken Institute pointed out, “Longevity is linked to location.”2

It’s not too surprising to learn a wealth of factors, including education, income, access to health care, food choices, smoking rates, exercise, the safety of housing, and pollution, affect life expectancy and quality of life. However, the cities that provide the best environments for aging in place may be unexpected.

For 2017, the report identified these large cities as the best for aging in place:2

[/caption]

While southern migration has played a role in many retirements, the Milken Institute suggests today’s retirees may be seeking a different type of retirement experience. “They are launching companies and nonprofits, climbing mountains, creating apps, and mentoring youth. They increasingly seek lifelong engagement and purpose.”2

Often, older Americans are finding these experiences close to their hometowns. While many retirees move, most – 60 percent on average – land within 20 miles of their previous homes. They tend to remain close to family and friends and age in familiar communities. Just one-fifth move more than 200 miles away, according to the Center for Retirement Research at Boston College.3

Those who settle farther from home may choose their destinations because they offer engaging programs and valued amenities. In its 2017 report on the Best Cities for Successful Aging, the Milken Institute pointed out, “Longevity is linked to location.”2

It’s not too surprising to learn a wealth of factors, including education, income, access to health care, food choices, smoking rates, exercise, the safety of housing, and pollution, affect life expectancy and quality of life. However, the cities that provide the best environments for aging in place may be unexpected.

For 2017, the report identified these large cities as the best for aging in place:2

]]>

]]>

Posted on January 02, 2024

Posted on December 18, 2023

Posted on December 11, 2023

Posted on December 04, 2023