Market Insights:

January 2, 2024

Posted on January 02, 2024

Planning and Guidance, Tailored To Your Life and Goals

Tuesday Takeaway

Posted on May 26, 2020

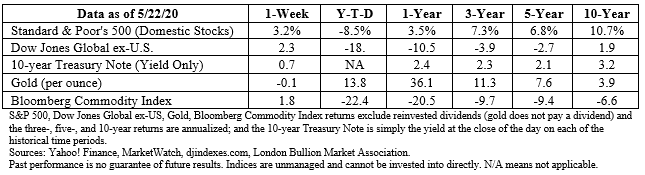

The Markets

It was a good week for stock markets in the United States, but there was trouble in Asia.

U.S. stock markets rallied last week. The Dow Jones Industrial Average, Standard & Poor’s 500 Index, and Nasdaq Composite all gained more than 3 percent, reported Ben Levisohn of Barron’s.

Investors had plenty of fuel for optimism early in the week. On Sunday, Federal Reserve Chair Jerome Powell struck a positive tone during his 60 Minutes interview stating, “The big thing we have to avoid…is a second wave of the virus. But if we do, then the economy can continue to recover. We’ll see GDP move back up after the very low numbers of this quarter. We’ll see unemployment come down. But I think though it’ll be a while before we really feel well recovered.”

On Monday, there was news early testing of a potential vaccine had delivered promising results, and the vaccine company’s stock shot higher. The report was tarnished when top executives sold shares the next day, and a respected medical website indicated the published results meant little, reported John Authers in Bloomberg Opinion.

Positive momentum slowed later in the week when China indicated it will impose national security laws on Hong Kong. Reshma Kapadia of Barron’s reported, “While the risks have ratcheted higher, it isn’t clear yet whether the new security laws will destroy Hong Kong’s ability to act as a financial center. What that could mean for investors will probably play out over the next couple of months.”

Hong Kong’s Hang Seng index closed down 5.6 percent, reported Financial Times (FT). That was the index’s worst one-day performance in almost five years.

China’s leadership also declined to set a gross domestic product (GDP) target for the first time ever. GDP is the value of all goods and services produced in a nation. The decision led to a decline in mainland China’s CSI 300 index of Shanghai and Shenzhen-listed stocks, reported FT.

“The pessimistic one is front-end corporatization: small businesses just evaporate, their real estate is taken over by big companies, and (some of) their employees find new jobs at these companies…Here’s the good one. Those same local businesses are running down their cash reserves, but lenders are banging down the door with a crazy offer: borrow enough to meet payroll now, pay nothing – until business starts coming back…[Lenders get] more involved in the borrower’s business – get them good bookkeeping software and a modern point-of-sale system. Band together a bunch of borrowers and start negotiating with suppliers and landlords. In short, use software economics to give small businesses the same economies of scale that large ones already benefit from.”It’s possible we could see both situations occur.]]>

Posted on January 02, 2024

Posted on December 18, 2023

Posted on December 11, 2023

Posted on December 04, 2023