Market Insights:

January 2, 2024

Posted on January 02, 2024

Planning and Guidance, Tailored To Your Life and Goals

Tuesday Takeaway

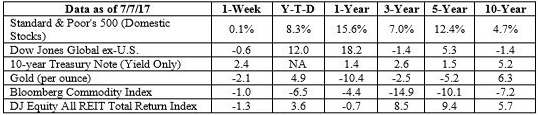

Posted on July 11, 2017

| “…S&P financials have gained some 6 percent, with tech sliding almost 4 percent. That still leaves financials lagging behind the S&P 500 for the year and well behind the roughly 17 percent gain for tech. A similar story has unfolded in Europe between banks and tech.” |

| “Several Wall Street giants have warned of weak trading revenue in Q2, continuing the lackluster trend in 2017…Still, bank stocks large and small have been leading in recent weeks, helped by higher bond yields and massive buyback and dividend plans.” |

| “…typical households in most of America’s larger cities don’t earn enough to afford the average new vehicle, under a common budgeting rule for buyers… The ‘20/4/10’ rule says you should aim to put down at least 20 percent of a vehicle’s purchase price, take out a car loan for no longer than four years, and devote no more than 10 percent of your annual income to car payments, interest, and insurance. If you can’t stay within those lines, you can’t afford the car.” |

| “…millions [of] cars that were leased two or three years ago, many of them used compact and midsized cars with low mileage, are heading toward auction lots and used car dealerships. That surge in supply threatens to depress prices for new and used vehicles, raising the risk of losses for automakers and finance companies on lease deals. It also undercuts the value of cars customers want to trade in for a new vehicle.” |

Posted on January 02, 2024

Posted on December 18, 2023

Posted on December 11, 2023

Posted on December 04, 2023